#7 - Income Taxes in Ireland (Part 2)

Understanding the difference between marginal and effective tax rates

Our previous article on Income Taxes in Ireland has proved popular. But many people confuse the total amount of tax they pay (effective tax rate) with the tax they pay on extra income (marginal tax rate). It’s really important to know the difference…

Most people agree that those who earn more should pay more tax and Ireland’s tax system is structured exactly like this. If you only earn €10k a year you’ll pay no tax, but if you make €100k you will pay a lot (roughly €38.5k actually).

The tax system lets those on low incomes keep all (or most) of their earnings, but takes an ever-increasing slice from those with higher incomes. This is what a marginal tax rate means - the tax rate on earnings ABOVE a certain threshold. For example with USC, you pay nothing on your first €12k of income and 0.5% of income above this. So if you make €15k, you’ll pay 0.5% on €3k of earnings, not on the full 15k. Similarly, if you’re making €12k and get a raise to €12,100 you’ll pay tax only on the extra €100 and even then it will only be a tiny amount.

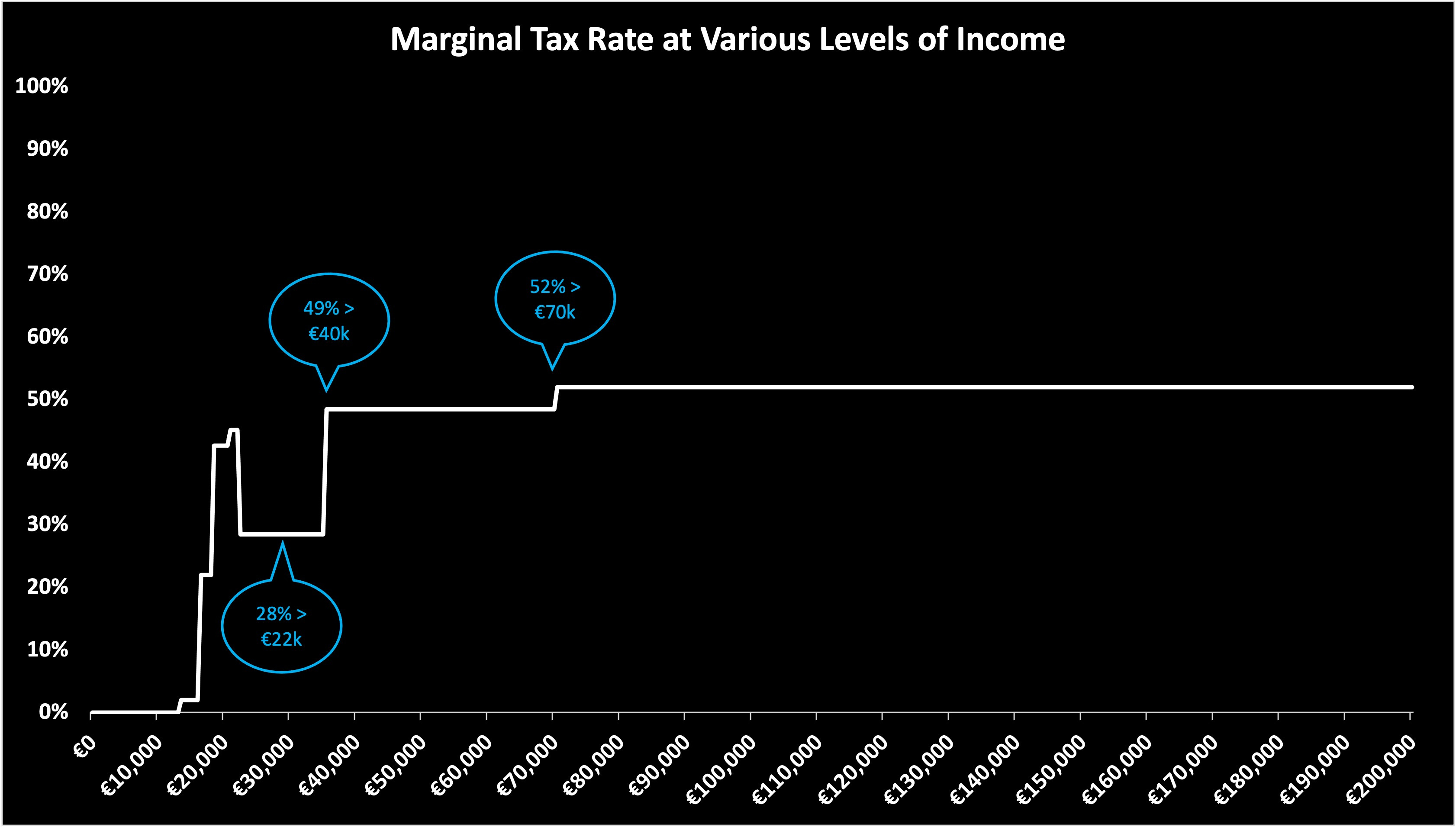

The entire tax system works on this principle, although it can more complicated when Income Tax, PSRI, USC and ASC are each added in. The graphic below shows how the marginal tax rate increases as you earn more. While the graph has a small peak at incomes around €20k (see footnote1), it rises to a 28% marginal tax rate on incomes above €22k, 49% on incomes above €40k and a massive 52% on incomes above €70k. (For the record, it’s even higher for public sector workers due to the ASC)

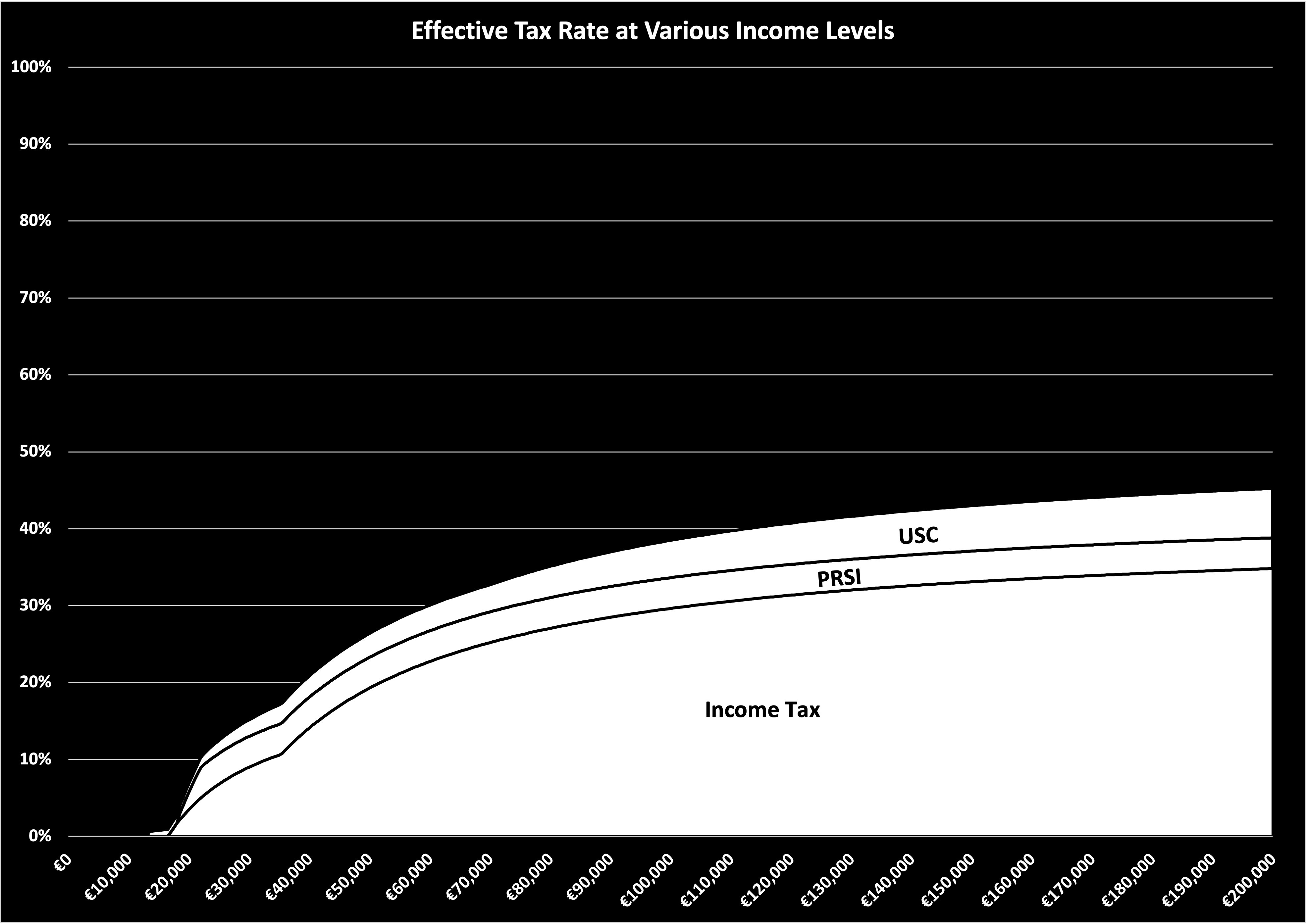

So how does this affect the total amount of tax you pay? For most full-time workers you’ll pay no tax on some of your income, some tax on a portion, and a higher rate on the rest if you’re well paid. When these slices are blended together it gives you the total, or ‘effective’ tax rate on a certain level of income. This is what it looks like.

So what does it all mean?

Firstly, you will ALWAYS be better off with higher income. We occasionally hear of someone turning down overtime because they mistakenly believe they won’t keep any of the extra income if it pushes them into a higher tax bracket. This is just wrong. In the worst case scenario, even if you’re already in the highest tax band, you’ll keep at least 48% of your extra earnings.

A tax system is described as progressive when the tax rate rises quickly on higher incomes. As is clear from the above, Ireland’s tax burden rises very rapidly and is actually the most progressive tax system in Europe.

It’s noteworthy how high the tax burden is on those with average and high incomes. Our 52% highest marginal tax rate is high in international terms, but it is even more unusual that it kicks in at a relatively low level of earnings (in an international context).

Please subscribe so you don’t miss any future articles explaining more of these topics in simple terms (mortgages, pensions, taxes, and ways to help reduce your taxes), and follow us on twitter to continue the conversation or ask any follow-up questions.

The peak in marginal tax rates is explained by PSRI. You don’t pay any PSRI on income below €352 per week (€18.3k) and you pay 4% on all earnings above €424 per week (€22k). This explains the peak in this area of the graph, noting that the impact of the PSRI credit ensures that the marginal tax rate remains below 50% over this range.

Fantastic article, thank you.

Wanted to ask if possible if you could cover taxes on stocks and bonuses? I think if I remember correctly they are pretty high rates.

Thanking you,

Abdul